UK insurer Hastings announced its intention to float on the London Stock Exchange on Tuesday, with a 180 million pound ($277.78 million) share sale aimed at accelerating its growth.

The offer to institutional shareholders is expected to result in admission to London's premier stock market in October, the company said in a statement.

Hastings, one of Britain's fastest growing motor insurers, is expected to be eligible for inclusion in FTSE UK indices.

Goldman Sachs Investors will retain a significant indirect shareholding following the floatation and will remain Hastings' largest shareholder following completion of offer. ($1 = 0.6480 pounds) (Reporting by Emiliano Mellino, editing by Sinead Cruise)

In Darego v AG Leventis Nigeria Limited the Lagos Court of Appeal reaffirmed an exception to the common law position that a third party cannot join an insurer in a suit against the insured in respect of an insured risk.(1) One of the major issues for determination was whether the lower court was right to dismiss the claim against Great Nigeria Insurance Co Limited (the third respondent in the suit) on the grounds that there was no privity of contract between it and the claimant Betty Darego.

Previously, an insurer could be joined as a party only through a separate third-party proceeding, as it was believed that there was no privity of contract between the third party and the insurer. However, the appeal court found that an exception to the common law position had been established in accordance with Section 11 of the Insurance (Special Provisions) Decree (40/1988).

Facts

In 2001 Darego's vehicle, a Mercedes Benz 230, was involved in an accident with a vehicle belonging to Mr Ogundiyan (the fourth respondent). Ogundiyan accepted liability and submitted a copy of his third-party insurance policy with Great Nigeria Insurance Co Limited to Darego with a view to getting her car repaired.

However, after taking possession of Darego's car for repairs, AG Leventis Nig Ltd and Leventis Motors (the first and second respondents in the suit, respectively) failed to repair or return the vehicle to Darego.

Darego filed a claim at the lower court against both the insured and the insurance company for:

either:

the immediate return of her car; or

N7 million (the value of the car as of December 2002);

transport expenses of N2,500 per day from June 23 1999 until the date of full payment of damages; and

N10 million in general damages.

The lower court found that Darego's car had been illegally and unlawfully converted and entered judgment in her favour. However, it refused to award most of the damages sought by Darego. Darego appealed the lower court's refusal to award damages.(2)

Decision

One of the issues that the appeal resolved was whether the lower court was right in finding that there was no privity of contract between Darego and Great Nigeria Insurance Co Limited, which was not privy to the illegal conversion of the car and thus could not be held liable for the alleged loss suffered by Darego.

The appeal court stated that although under common law a third party cannot join an insurer, the position had since changed by virtue of Section 11 of the Insurance (Special Provisions) Decree. Section 11 provides that:

"Where a third party is entitled to claim against an insurer in respect of a risk insured against, he shall have a right to join the insurer of that risk in an action against the insured in respect of the claim; provided that before bringing an application to join the insurer, the third party shall have given to the insurer at least thirty days' notice of the pending action and of his intention to bring the application."

In arriving at its decision, the appeal court relied on an earlier decision in Unity Life and Fire Insurance Co v Ladega.(3) In this case, the court took into account the intention of the lawmakers at the time of promulgation of the decree. The court was of the view that Section 11 of the Insurance (Special Provisions) Decree allows the insurer to be joined only as an indemnifier for any judgment obtained against the insured in a claim against the insured. Therefore the third party's right to join the insurer is to enable the third party have direct access to the insurer instead of waiting for judgment to be given before asking the insurer to settle the claim.

Comment

This decision is a welcome development to Nigeria's insurance jurisprudence. A third party can now join an insurance company in a suit against the insured on fulfilling the preconditions in Section 11 of the Insurance (Special Provisions) Decree (ie, issuance of a mandatory 30 days' notice of intention to join the insurance company).

This article was first published by the International Law Office, a premium online legal update service for major companies and law firms worldwide. Register for a free subscription.

The Nigerian insurance sector is witnessing a paradigm shift with major developments changing the face of the insurance market in the country. Through the instrumentality of the National Insurance Commission (NAICOM), some reforms were instituted, coupled with fundamental partnerships. To this effect, the sector is projected to take over the helm of affairs of the industry in Africa within the next few years.

Before now, several challenges had bedeviled the insurance industry and threatened its existence. At the initial stage, many Nigerians did not understand the industry. The quota the sector contributed to the country’s GDP at a point was below 1%, prompting the government’s minimal recognition of the industry as an efficient contributor to the financial sector. There was also a low awareness of the need for insurance for the public. In addition to this was a poor regulatory framework and inevitably, the public, (which was supposed to be the insurance market), lost confidence in the sector.

However, since NAICOM, the industry regulator rolled out a series of reforms, the sector has undergone remarkable transformations with the introduction of Market and Restructuring Initiatives (MDRI). Some of the other reforms include risk based supervision, migration to International Financial Reporting Standard (IFRS), market conduct reforms, claims settlement reforms and financial inclusion.

The reforms have recorded significant impacts for the sector. First in line is the attraction of foreign investors and emergence of strategic partnerships. A very strong indication of this is the investment of Old Mutual insurance firm in Oceanic Insurance, Sanlam Group in First Life Insurance, Assur Africa Holding, and an association of three European Development Finance Institutions (DFIs).

Equally, there is a boost in the confidence of Nigerians and the government’s recognition of the sector that currently boasts of its credibility. Public confidence ultimately means a high patronage from the most populated African country- the main reason foreign investors took interest in the sector.

The most significant reform, which earned the trust of the public came in 2005, is the recapitalization policy. This reviewed upwards the capital base of life assurance companies to N2 billion from N150 million and N3 billion from N200 million for general insurance businesses. It reduced the number of insurance firms from 103 to 49, but however increased their capacities to accept and retain risks- meaning more efficiency.

NAICOM’s reform on migration to IFRS has resulted in better financial discipline of firms. The no premium no cover policy has been working for the benefit of both the insurer and the insured.

Although challenges are still prevalent, better opportunities remain that can place the industry on a global ranking. The continued performance of these reforms is largely dependent on NAICOM’s ability to consistently grease the wheels of reforms and provide the support the sector needs to achieve its full potential.

The Company secretary, legal advisers 2015 summit has been postponed.

A statement from the organisers said the postponement was

due to the Sallah holiday. The event which was earlier scheduled for September

22 to 24, has been moved to Monday 28 to Wednesday 30 September 2015.

The venue remains Park Inn by Radisson, Abeokuta Ogun State.

For registration, send nominations to adepegbachambers@gmail.com or

Adegboyega Adepegba & Co Plot A12 Gbagada Oshodi Expressway Gbagada, Lagos.

Call Ade on 08033052304 or 08055312548

At less than 3 per cent insurance penetration rate, Rwanda is one of the countries with the lowest insurance uptake levels in the region. Many stakeholders and pundits have always blamed this state of affairs on lack of awareness about the importance of insurance among the public. However, some experts say the problem goes deeper, and partly blame insurance companies for being short on creativity and innovation to develop products that are market and sector-specific. Sector players also blame lack of enough professionals in the insurance industry as another contributing factor to the low levels of insurance penetration in the country. According to Jean Pierre Majoro, the executive secretary of the Association of Insurance Companies in Rwanda, insurers have ignored some of the sectors in the economy, like the small-and-medium enterprises (SMEs), which could spur policy uptake if they were targeted. Majoro challenged insurance firms to develop tailor-made products for specific sectors. Agriculture, one of the key drivers of the economy has largely been neglected by insurers, who claim it is too risky presently. However, Majoro says insurers should create micro-insurance products, targeting SMEs and the agriculture industry, arguing that this approach could help change the tide and make the industry more competitive. "Micro-insurance is ideal for our market and could help increase insurance penetration in the country if sector players embrace it. The regulator has already put in place an enabling policy. It is up to insurers to take advantage of this and invest in skills development to propel innovation among staff so that they are able to create insurance products that suit all market segments," Majoro told Business Times. He added that insurance companies need to analyse the ongoing activities in the informal sector and develop products accordingly. Insurers are lobbying for the establishment of a professional school of insurance as one of the ways to help boost skills in the sector. They also want to see insurance incorporated into the national school curriculum, from secondary level. This, according to Dr Blaise Uhagaze, the secretary general of the Association of Rwanda Insurers, will help increase the skills pool and eventually make the sector more competitive locally and in the region. 'SMEs reluctant' Esdras Nkundumukiza, the commercial director in charge of SMEs at SORAS, a local insurance company, said though there are already products tailored for their needs, many of them are reluctant to take up policies to cover their businesses. Nkundumukiza noted that many of the local SMEs think insurance is not important for small businesses. He challenged SMEs to embrace insurance, saying it is a fall-back in case of calamities, like when a fire guts their businesses as was the case last year, when dozens of SMEs lost their merchandise in fire in different parts of the country. "We conducted a number of campaigns on micro-insurance products, but the response was poor. It is, therefore, important for the informal sector to work with insurers and safeguard their enterprises. This is a win-win for both the SMEs and insurers," he argued. Rwanda's insurance sector recorded a 19 per cent increase in total assets during the first half of the year, hitting Rwf295 billion, up from Rwf247 billion in June last year, and Rwf272 billion as at the end of December. The sector's capital and reserves grew to Rwf218 billion, from Rwf180 billion over a similar period in 2014, which was an increase of 21 per cent. However, sector experts believe the performance could have been far better, if market players were innovative or embrace new tools, including Information and Communication Technologies (ICTs), according to Majoro. Experts say insurance is essential for the country to achieve double digit growth figures by 2018, under the second Economic Development and Poverty Reduction Strategy (EDPRS II). The sector is comprised of insurance and pension institutions, including eight non-life insurers, four life insurers, two public medical insurers, 14 insurance brokers, 322 insurance agents, nine loss adjusters, as well as one pension/social security fund, Rwanda Social Security Board, and 53 private pension schemes. Sangono Kagaba, the director for non-banking institutions supervision at the central bank, said the country's insurance industry is still young, with a lot growth potential that the private sector should exploit to expand and become more profitable. "The central bank supervision of the sector has increased public confidence, resulting in the growth of the sector registered in recent times. It has also been able to acquire long-term resources and, consequently, helped strengthen the country's capital market," he said. Price undercutting tamed Meanwhile, the National Bank of Rwanda and the insurance sector players are working together to address the challenge of price undercutting. According to John Rwangombwa, the central bank governor, the practice that had slowed the sector's profitability the previous year "has been brought under control". "We have worked with the association of insurers to fix the issue, and I can now say that the situation has improved," Rwangombwa said.

The wife of a Cleveland firefighter conspired with a group of young

men to kill her husband so she could collect on a life insurance policy

and cover up financial fraud she committed in her husband’s name,

prosecutors said Monday.

Uloma Walker-Curry, 44, was indicted on aggravated murder, conspiracy

and felonious assault charges in the November 2013 slaying of fire Lt.

William Walker, 45, the Cuyahoga County Prosecutor’s Office announced.

He was shot to death in the driveway of his Cleveland home. Chad

Padgett, 21, Christopher Hein, 22, and Ryan Dorty, 23, were indicted on

the same charges.

Walker-Curry asked Padgett and a juvenile to kill her husband,

prosecutors said. They allege Padgett then recruited his cousin, Hein,

who turned to Dorty, who killed Walker.

Cleveland homicide detectives initially followed leads provided by

Walker-Curry that neighborhood drug dealers might have killed her

husband to stop him from complaining about them. But a Crime Stoppers

tip and cellphone technology, including text messages, led detectives to

investigate Walker-Curry, who was arrested last week, prosecutors said.

Dorty was sentenced to 15 years in prison last year for an unrelated

aggravated robbery. Padgett was arrested Aug. 8 for Walker’s slaying.

Padgett dated Walker-Curry’s daughter, prosecutors said.

No attorney information was available for the four suspects.

Walker-Curry and Padgett are being held on $1 million bonds. No bond has

been set for Hein, who was arrested Monday. The juvenile will

eventually face delinquency charges, prosecutors said.

Connected, communicating devices, often referred

to as Internet of Things could be one technology to revolutionize the

industry. (Shutterstock/nopporn)

Insurance companies talk about new product development and

speed to market, but true innovation is rare in the insurance sector.

However, connected, communicating devices, often referred to as Internet

of Things (IoT) could be one technology to revolutionize the industry.

Sensors offer unprecedented access to granular data that can be

transformed into assessing risk more accurately. For many insurers their

initial exposure to IoT has been via telematics devices. But today

sensors are used in thousands of different devices. Sensors are used in

buildings and bridges to monitor for structural defects and mitigate

potential losses. Life insurance companies are using the data from

wearable devices like FitBit and Nike+ FuelBand to better assess the

health of the life insured. And, sensors are being implanted into

animals to track and identify livestock, helping insurers rate and price

agricultural insurance more accurately. Related: 4 steps to building a strategic analytic culture in your organization

The first sensors appeared decades ago, but in the last five years

two major changes have shaken the sensor world and caused the IoT market

to mature. From a technology perspective, the size and cost of the

devices have decreased dramatically, and Wi-Fi and wireless

communications make it more efficient to transmit the data.

In an industry that’s frequently slow to adopt cutting-edge

technologies, IoT is starting to make waves. To successfully leverage

IoT, insurers need to invest heavily in both data management and data

analytics. Data management

Big data has become a technology buzzword, and it is at the heart of

IoT. First of all, let’s consider the amount of data that automotive

telematics devices are expected to generate. A telematics device will

produce a data record every second. This data record will include

information such as date, time, speed, longitude, latitude, acceleration

or deceleration, cumulative mileage and fuel consumption. Depending on

the frequency and length of the trips, these data records or data sets

can represent up to 1 GB of data per day, per vehicle!

To store this data, many insurance companies use distributed

processing technologies such as the Hadoop file system. Hadoop is an

open-source software framework for running applications on a large

cluster of commodity hardware. Since Hadoop runs on commodity hardware

that scales out easily and quickly, organizations are now able to store

and archive a lot more data at a much lower cost.

By Gloria GrandoliniSenior Director of Finance & Markets Global Practice at the World Bank Group

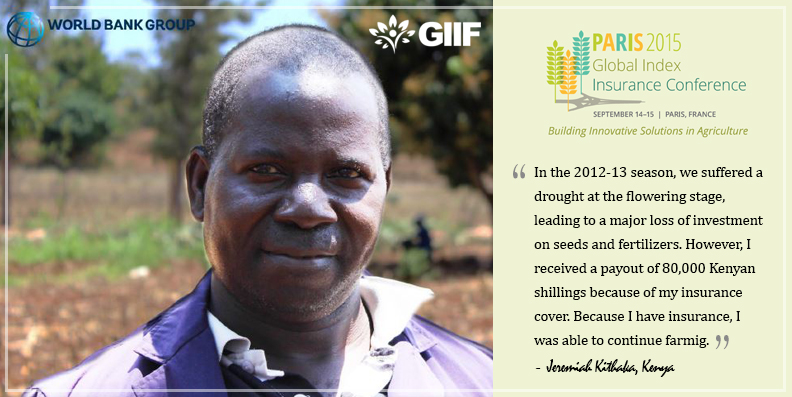

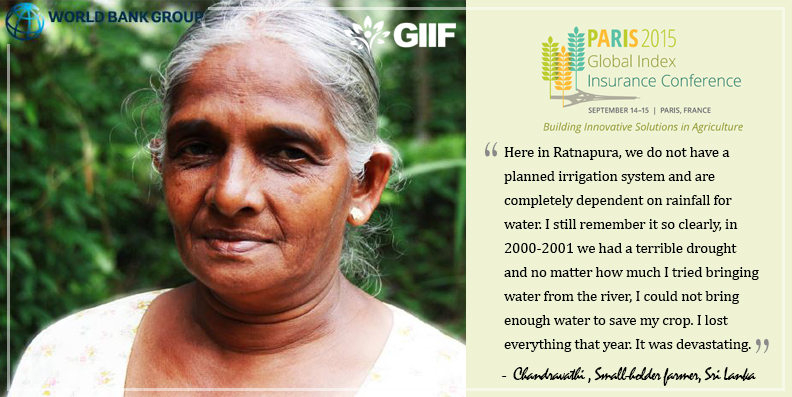

Insuring crops against unforeseen weather events is a standard practice among farmers in rich countries.

Traditional

insurance is either unavailable or is very expensive in many developing

countries, leaving small farmers particularly vulnerable.

A

severe drought, a devastating earthquake or another weather disaster can

wipe out small farmers. Such uncertainties also make them more risk

averse and less likely to invest in their farms.

Since

the traditional individual and group-based underwriting and

indemnity-based products aren't serving developing countries, index

insurance is an alternative approach more suitable to insuring poor

farmers in hard to reach areas. Index insurance

pays out benefits based on a predetermined index for loss of assets and

investments resulting from catastrophic events, unlike traditional

insurance which depends on insurance claims assessors to evaluate the

damage. A statistical index is developed before the start of the

insurance period to measure deviations from normal for such parameters

as rainfall, temperature, seismic activity, wind speed, crop yield or

livestock mortality rates.

This approach can help stabilize poor

farmers' income, allowing them to continue farming regardless of

disaster and weather uncertainties.

A global conference on index insurance

is underway in Paris this week, bringing together development partners

and the private sector to discuss how to expand index insurance to

address the growing risks and impacts of climate change and natural

disasters.

Rising climate change risks and weather-related losses

could have a devastating impact on the world's most vulnerable

populations over the next generation.

Weather-related

losses and damage have risen from an annual average of about $50

billion in the 1980s to close to $200 billion over the last decade,

according to the World Bank's report The Building Resilience: Integrating Climate and Disaster Risk into Development.

While index insurance can't shield agriculture from climate change, it can help mitigate its effects.

Insurance

can also help to decrease the financial vulnerability of billions of

people, providing them with a means to access finance and credit.

We need to dramatically scale up work in this area and find innovative

approaches to increase insurance coverage to the most under-served and

vulnerable populations.

On average globally, approximately

one-third of the claims from total man-made and natural disasters are

covered by insurance, according to Swiss Re estimates.

However,

the coverage varies greatly from developed to developing countries. For

example, for the 1999 floods in Austria, Germany and Switzerland, 43%

of damages were covered by insurance while only 4% of damages from

floods in Venezuela were covered in the same year. Only 10-15% of the

losses after Typhoon Yolanda in the Philippines were insured, compared

to 50% for the losses from Hurricane Sandy in the United States.

The World Bank Group

has been pioneering different types of index insurance products. With

donors support, our work has led to more than 35 million farmers

benefiting from new or improved index insurance products over the last

10 years.

While new insurance products in emerging markets offer

growth opportunities for the insurance industry, commercial success

won't happen overnight. It can take between 10 to 15 years to make these

markets commercially viable.

This is why governments and

foundations should also champion and promote risk-management solutions,

and contribute capital during the incubation period.

This week's index insurance conference

is a call for dialogue and ideas, and for building stronger

partnerships with the private sector to promote innovations, especially

in agriculture insurance.

There

are challenges associated with building sustainable and scalable

insurance markets in developing countries, including uneven population

distribution, poor infrastructure, and a lack of reliable data. But

these challenges shouldn't hold us back from finding new approaches to

extending insurance to the most vulnerable.

Ensuring the

sustainability of food production, especially in the poorest countries,

is critical to fighting hunger, tackling malnutrition and boosting food security for the world's population that is expected to reach 9 billion by 2050.

Without

bold action now, the warming planet threatens to put prosperity out of

reach of millions of people and roll back decades of development

progress.

The first sensors appeared decades ago, but in the last five years

two major changes have shaken the sensor world and caused the IoT market

to mature. From a technology perspective, the size and cost of the

devices have decreased dramatically, and Wi-Fi and wireless

communications make it more efficient to transmit the data.

The first sensors appeared decades ago, but in the last five years

two major changes have shaken the sensor world and caused the IoT market

to mature. From a technology perspective, the size and cost of the

devices have decreased dramatically, and Wi-Fi and wireless

communications make it more efficient to transmit the data.